How Insurance Uses Location Data to Prepare for Natural Disasters

Insurance providers must move quickly to take advantage of the location data available to them. Confronted with a world with more extreme weather than ever before Location Intelligence is helping insurers prepare their organizations and policyholders for the inevitable increase in natural disasters and extreme weather events.

According to Gartner only 30% of insurance industry organizations are utilizing Geospatial and Location Intelligence.

Embracing Location Intelligence can help insurers to reduce their exposure to risk while preparing and offering policyholders better service and more varied plans that meet their needs.

Staying up to date with real-time mapping

During a disaster event it is imperative for insurance companies to be as informed as possible.

By viewing data and risk exposure in real-time a company is best equipped to adapt and quickly address the needs of the policyholders that are most adversely affected.

The map below shows a projected hurricane track off the coast of Florida paired with policyholders data. The map (which could be updated with NOAA data in real-time during a real hurricane event) shows which policyholders are at risk of hurricane damage and the amount of that damage.

Tracking a storm or event and its impact on your policyholders can also assist in resource and personnel distribution to an impacted area making sure that you have the right number of claims adjusters on the ground to assess damages.

The savvy insurance agency can also use spatial analytics to determine outliers in claims and investigate fraudulent cases helping insurers focus efforts on customers that actually require assistance.

Helping consumers to understand and mitigate new risks with diverse policy options

Diversifying policy options is imperative to spreading out risk exposure while protecting policyholders who may not even recognize new challenges and dangers.

Estimates show that 60% of homes affected by Hurricane Irma and 80% of homes affected by Hurricane Harvey were uninsured against the damages.

Since flood insurance is not traditionally included in a standard homeowners insurance policy insurers should be proactive in informing their policy holders of their risk regardless of where they fall on a floodplain map or other risk assessment.

A report from ClimateWise a coalition of insurance industry organizations has identified a huge jump in “the protection gap” or the difference between the total costs of natural disasters and the amount insured against the damage which has quadrupled since the 1980’s to $100 billion/year.

With cheaper or more diverse policy options for those medium- to low-risk customers (that are newly exposed to risk due to global climate change) insurers can protect more property owners and spread out the risk they hold.

Update outdated maps and conceptions with varied data sources.

To get a full picture of the inherent risk associated with using outdated resources we can look at the example of FEMA’s 100 year Floodplain map.

Federal law dictates that flood insurance is required for properties that fall within a high flood risk zone although the determination of what constitutes high risk is based of the FEMA’s 100 year floodplain map which can be a bit problematic.

First the 100 year floodplain map is out of date and new flood mapping is expensive and challenging.

FEMA is making constant updates to their maps but over 20 000 communities across the United States fall under their purview as possible flood risks.

FEMA is forced to prioritize updates based on cost benefit as well as the recency of their last update which can leave cities to base critical disaster relief plans based on old data. Often even when newly updated these maps can lack information on local development which can have substantial impact on flood risk and almost all of them ignore the impact of global climate change.

Second the 100 year floodplain map is misunderstood by the general public.

Just based on the name even an informed consumer may think that a property falling within the 100 year floodplain is likely to be flooded once every hundred years but in truth the map is identifying areas that have at least a 1% chance of flooding each year.

Houston for example has had what FEMA may consider a hundred year flood in each of the last three years.

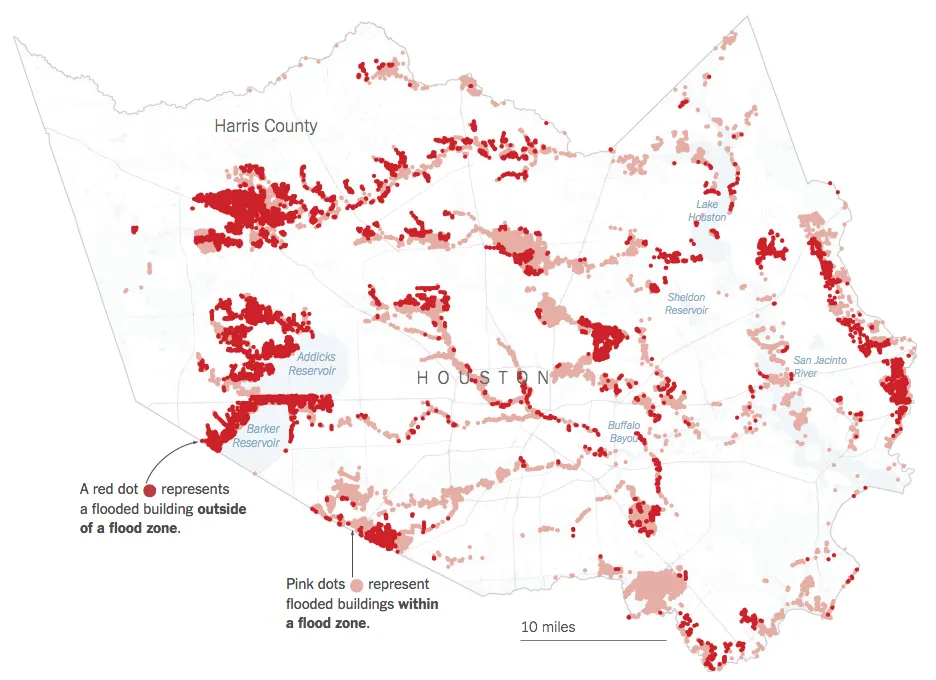

You can also see in the image below from the New York Times a high percent of the damage caused by flooding is coming from well outside both the 100 and even 500 year floodplain map risk zones.

Source: New York Times

Due to the inaccuracies that may be inherent in many traditional risk assessment tools Insurers should also be drawing on past claims data and open data sources to amend their understanding and properly assess flood risk. By visualizing more complete data insurers can help make sure that their customers are appropriately covered.

Use Location Intelligence to provide fair accurate and bias-free policy pricing to consumers.

There may be nothing more important to an insurance company’s long term health than having properly priced policies.

If an underwriter improperly assesses the risks associated with a particular property the pricing for that policy will be off. If that pricing is too aggressive (too low) an insurance company is opening themselves up to greater risk and the chance that a high number of claims would cut into earnings.

If policy pricing is too conservative a company risks getting undercut and priced out of the market.

Underwriters develop expertise in understanding and assessing risks and base their assessments and policy pricing on highly varied datasets.

By making sure that your underwriters are equipped with the most up to date tools and techniques you can reduce overall exposure to risk and prevent non-data driven bias from entering the process.

Contemporary Location Intelligence tools can synthesize multiple data sets and using spatial analysis provide the modern underwriter with deeper and more dynamic insights.

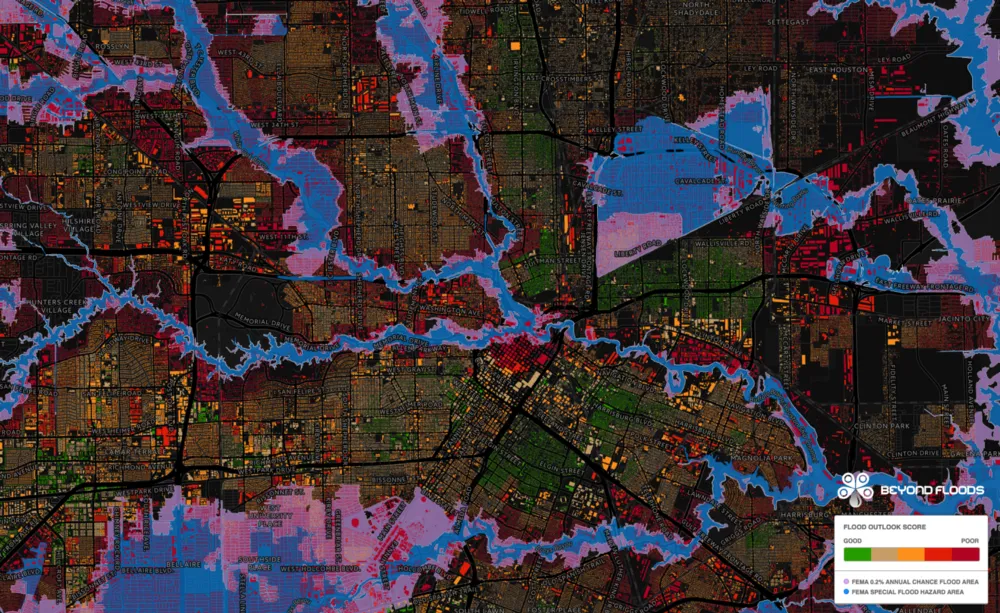

For example a tool like Syndeste’s BeyondFloods can act as a treasure trove for the underwriter looking to accurately assess a property’s flood risk using something more powerful than an outdated floodplain map.

In addition to providing a granular view of relevant and varied data points from public and private datasets BeyondFloods can create a comprehensive index or in their case ‘Flood Score’ as mapped above which can help underwriters to pinpoint the sweet spot for policy pricing.

Crowdsource data and build community to mutually benefit insurers and policyholders.

Building a strong and interconnected community may seem challenging and expensive in the insurance world but with benefits to both insurance companies and policyholders it should be a priority.

With smartphones in hand policyholders can become a real-time and insightful data source. Using a crowdsourcing platform like Fulcrum for example to gather real-time data can improve claims management and ease the burden on adjusters.

Your policyholders can also provide real-time insights during a major event showing rising water levels the spread of a wildfire or the impact of a tornado.

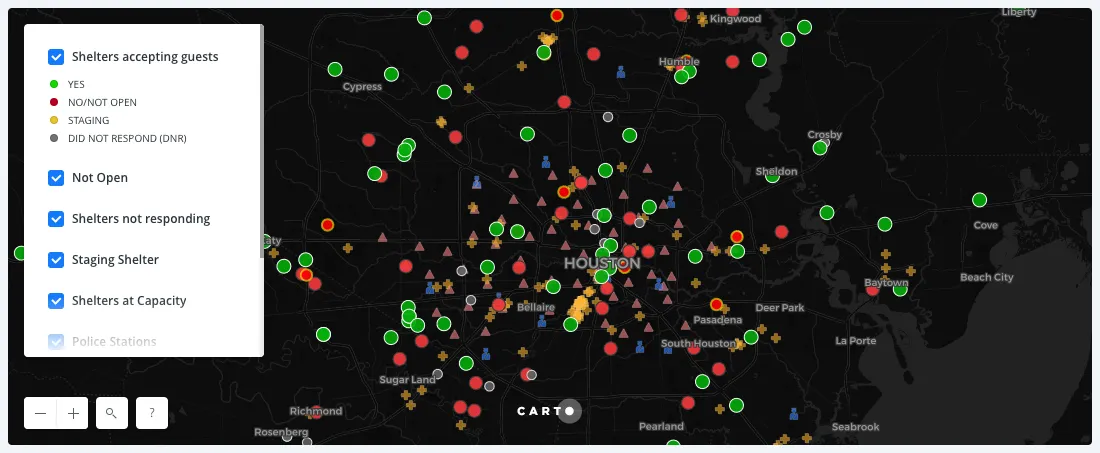

In the example below individuals collected data about shelter's statuses immediately following Hurricane Harvey in Houston in a google spreadsheet and mapped that data to show where shelters were and weren't accepting evacuees.

While independently anecdotal the full knowledge of an interconnected community can paint a clearer picture of risk exposure and allow more direct assistance from the insurer.

Adopting new technologies and methodologies around Location Intelligence is imperative for an insurance company that is looking to better connect with and protect their policyholders while maintaining their competitive advantage using fair and data-driven policy prices.